Argentina: Tightening of the foreign exchange control framework, increase of Corporate Income Tax, taxation of crypto currencies, & Supreme Court decision on interest deduction

1. New resolution limiting transactions of dollar denominates securities (General Resolution No. 907/21 of the ASEC)

In an attempt to reduce the drain of the Argentina Central Bank (“ACB”) dollar reserves and the continuous shortage of foreign currency, the Argentine Securities Exchange Commission (“ASEC”) issued General Resolution No. 907/21, which was published in the Official Gazette on October 6, 2021. Through this resolution, some new limitations on transactions in dollar denominated securities traded in Argentina – typically used by resident companies and individuals to circumvent foreign exchange controls – were introduced.

This new measure comes in addition to many others, already existing, which generally require (i) ACB approval for accessing to the Argentine foreign exchange market in order to exchange Argentine pesos for foreign currency either to save or to make transfer of funds abroad ̧and (ii) Argentine exporters to bring back to the country their export proceeds. Given such restrictions on many kind of cross border payments (i.e. dividends inclusive) certain alternative methods have become a common standard practice in the Argentine marketplace, like the exchange of pesos for dollar-denominated securities, which could be cashed abroad in foreign currency.

The new rules further restrict such peso for dollar-denominated security transactions. General Resolution No. 907/21 in particular, set forth the following:

- A limit of 50 thousand per week, considering their nominal value, in sales of securities denominated in dollars and issued under Argentine law with settlement in foreign currency (i.e. in tremors of market value it means approximately USD 19 thousand per week).

- Orders to enter into transactions in securities with settlement in foreign currency, or to transfer securities to or from foreign depositories may only be submitted if the following conditions are met:

(i) During the previous 30 calendar days, there were no sales transactions of securities denominated and payable in dollars, issued by the Republic of Argentina, under its local law, with settlement in foreign currency; and

(ii) A commitment to not perform the transactions defined in point (i), from the mo-ment in which the referred transactions are settled and for the following 30 consecu-tive days, is assumed. - The restrictions on the sale of securities denominated in dollars and issued under foreign law with settlement in foreign currency are terminated.

2. ACB Communication tightening the foreign exchange control framework (Communication “A” 7340/2021 of the)

In the same vein that the ASEC General Resolution No. 907/21, on 12 August 2021 the ACB issued Communication “A” 7340/2021 (“Communication 7340”). The first restriction relates to the impairment to pre pay imports of goods, in set case, during the next thirty days.

Secondly, it prohibits the settlement of purchase and sale transactions of securities with settlement in foreign currency through payment in foreign currency cash, or through their deposit in custody accounts or accounts of third parties.

Additionally, Communication 7340 provides that securities purchase & sale transactions settled in foreign currency (known as “cash with settlement”) must be paid by one of the following mechanisms:

- By transfer of funds to and from demand accounts held in the customer’s name with local financial institutions; or

- Against wire transfers on bank accounts in the customer’s name with a foreign entity that is not incorporated in countries or territories where the Recommendations of the Finan-cial Action Task Force do not apply, or do not sufficiently apply.

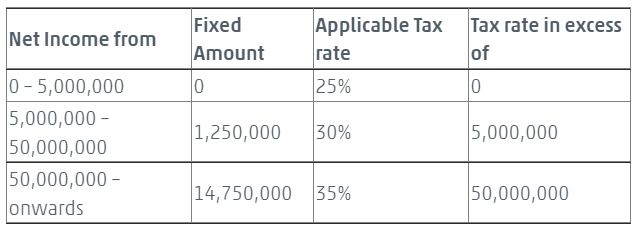

3. Reform of corporate income tax rates (law No. 27,630, published in the Argentine Official Gazette on June 16, 2021)

This law includes amendments to the Income Tax Law (“ITL”) in relation to corporate income tax rates applicable for fiscal years beginning on or after 1 January 2021, inclusive. The new regime incorporates a scale of rates with three differentiated brackets according to the level of accumulated taxable net profit. With progressive criteria, it was established the following:

All the amounts of the table are denominated in Argentina pesos (1 USD = 100,25 AR$).

These amounts will be updated considering the annual variation of the Consumer Price Index, published by the Argentine Census Bureau.

In all cases, the distributed dividends will be subject to a 7% tax rate. In this respect, please note that such tax rate is lower than the 10% cap for the taxation on dividends in the source jurisdiction, generally established in most Double Tax Conventions entered by the Republic of Argentina (15% in the case of the France-Argentina tax treaty).

4. New law to encourage savings and security transactions in local currency

In the previous context of limited dollar reserves at the ACB, the Argentine government enacted Law 27,638, published in the Argentine Official Gazette on August 4, 2021. This law introduces exemptions in the Income Tax and the Personal Property Tax, in order to encour-age savings and security transactions denominated in local currency (Argentine pesos) or in set domestic investments

- Income Tax (“IT”):

The exemption established by the ITL for certain kinds of interest is extended to interest payments resulting from the placement of funds through financial instruments issued in Argentine pesos, destined to promote productive investments, as defined in Decree No. 621/2021. - Personal Property Tax (“PPT”):

Certain financial instruments issued in Argentine pesos, are exempted from the PPT. Among the instruments exempted are the following:

(a) corporate bonds issued in accordance to Section 36 of the Argentine Corporate Bonds Law;

(b) financial instruments destined to promote productive investments, as defined in Decree No. 621/2021 and

(c) units or shares of mutual funds and financial trusts that (i) have been issued through a public offering authorized by the Argentine Securities Exchange Commission and (ii) whose underlying assets are comprised, at least, by a 75% of financial instruments mentioned above.

In turn, as mentioned above, the Decree No. 621/2021 sets forth the criteria to define the financial instruments included in those exemptions. Accordingly, it defines the term produc-tive investments as the direct or indirect investment in productive, real estate and/or infrastructure projects for different economic activities in the goods and services production sectors, such as agriculture, livestock, forestry, real estate, telecommunications, energy, logistics, fishing, science and applied research, among others.

5. Decree on taxation of crypto currencies (Decree No. 796/21, issued on November 17, 2021)

The Argentine Federal Government decided to include crypto currency transactions among those covered by the Tax on Credits and Debits in Bank Accounts (“TCDBA”). The TCDBA is a federal tax withheld by Argentine banks and other savings and payment institutions. It applies on any funds deposited that are either withdrawn or transferred from checking or savings accounts. The taxable base is the amount withdrawn or transferred, and the general tax rate is 0.6% on both debits and credits in bank accounts, or 1.2% on other set taxable events (e.g. organized systems of payments aimed at avoiding the use of local bank ac-counts), with limited exemptions. In order to tax crypto currency transactions, through Decree No. 796/21 an additional paragraph was added to Section 10 of the Annex to Decree No. 380/01, which provides for the TCDBA exemptions.

In fact, this new paragraph establishes that the exemptions of the TCDBA shall not be applicable to the movement of funds related to the purchase, sale, exchange, trading and/or any other transaction on crypto assets, crypto currencies, digital currencies, or similar instruments.

6. Argentine Supreme Court (“ASC”) ruling on interest deduction in the context of lever-aged buyouts (ruling “INC S.A.”, issued on July 15, 2021)

This ruling addresses the possibility of a Company to deduct from its CIT, interest derived from a debt contracted through the issuance of corporate bonds, when such debt is applied to the purchase of the shares of a third company. In fact, this was a case related to “lever-aged buyouts”, for it implies the acquisition of a company using a significant amount of borrowed money to pay the purchase price, followed by the use of such indebtedness in the operating business of the acquired company.

In this regard, the ASC decided to challenge the tax deduction of those financing interests. The highest court understood that – in this case – the issuance of corporate bonds was not destined at refinancing liabilities from productive activities that generate taxable profits, but at sustaining leverage, i.e., the purchase of a company taking debt, and then to absorb it and attribute the debt to the target company.

Therefore, according to the ASC, such interest is not deductible since it is not related to economic events taxed by the IT, and such relation is required by the ITL in order to allow any IT deduction.

If you wish to discuss these topics, please contact: Rosso Alba & Rougès, Buenos Aires

Writers: Cristian E. Rosso Alba and Sebastián de la Bouillerie, from Rosso Alba & Rougès

Original: https://wts.com/global/publishing-article/20220118-argentinia-fs-nl~publishing-article?language=en